Retirement Planning for 2026: Key Changes, Limits, and Smart Strategies

As we start **January 2026**, retirement planning gets a boost from new IRS limits and rules. The IRS increased contribution amounts for 401(k)s and IRAs, giving you more room to build your nest egg. Whether you're in your 20s starting out or nearing retirement, understanding these updates can help secure your future.

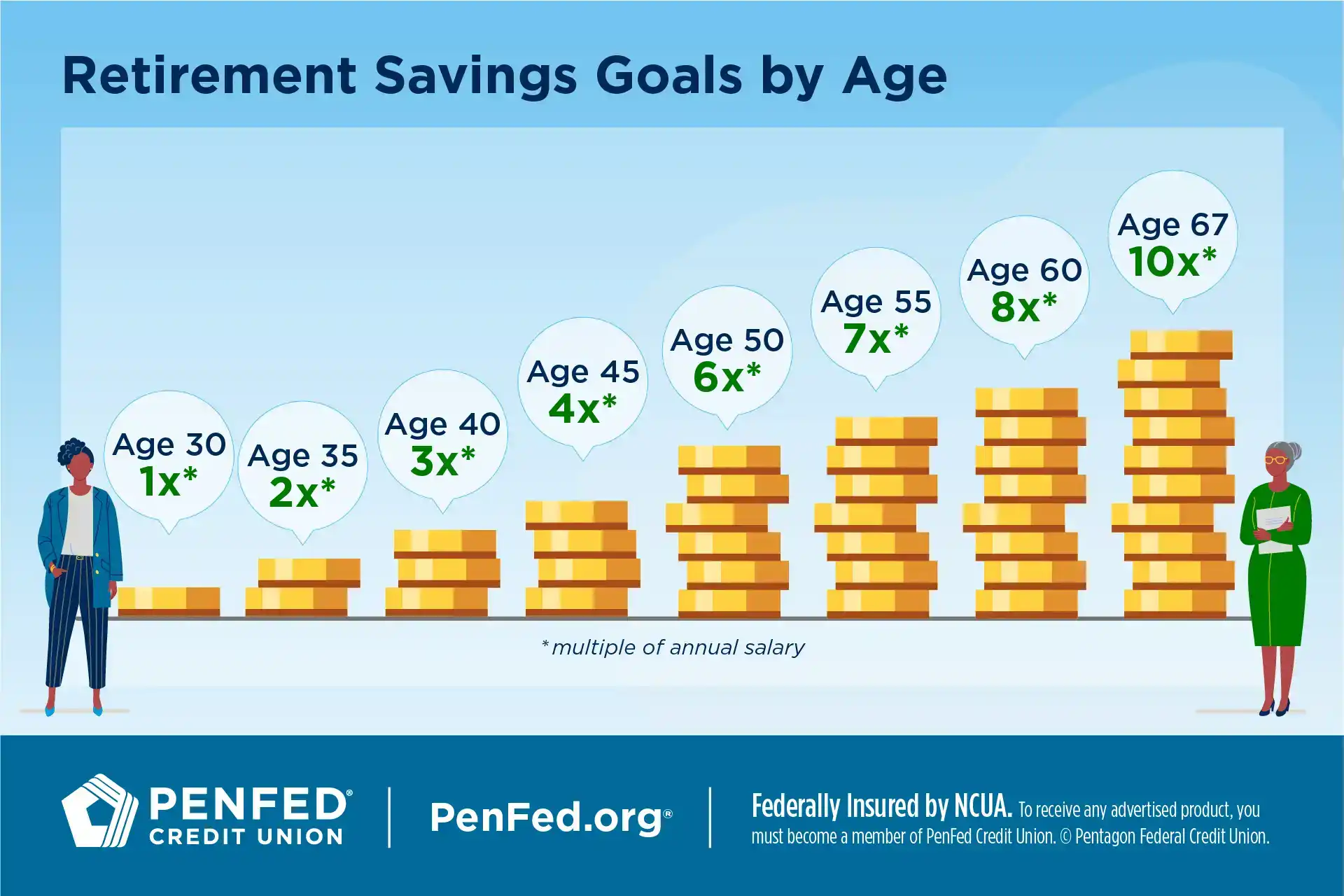

Retirement planning isn't just about saving—it's about smart tax strategies, maximizing employer benefits, and preparing for longevity. With Americans living longer, a solid plan ensures you enjoy those golden years without financial stress.

2026 Contribution Limits: Save More This Year

- 401(k), 403(b), most 457 plans, and Thrift Savings Plan: $24,500 (up from $23,500 in 2025).

- Catch-up for age 50+: Additional $8,000 (total $32,500).

- Super catch-up for ages 60-63: $11,250 (total up to $35,750 if plan allows).

- Traditional and Roth IRA: $7,500 (up from $7,000).

- IRA catch-up for age 50+: Additional $1,100 (total $8,600).

Note: High earners (over ~$150,000 in prior year wages) must make catch-up contributions as Roth (after-tax) in employer plans starting 2026.

Top Retirement Planning Tips for 2026

- Maximize Employer Matches: Always contribute enough to get the full match—it's free money!

- Prioritize Roth Options: With potential future tax changes, Roth contributions or conversions can provide tax-free growth.

- Automate Contributions: Set up automatic increases to hit the new higher limits effortlessly.

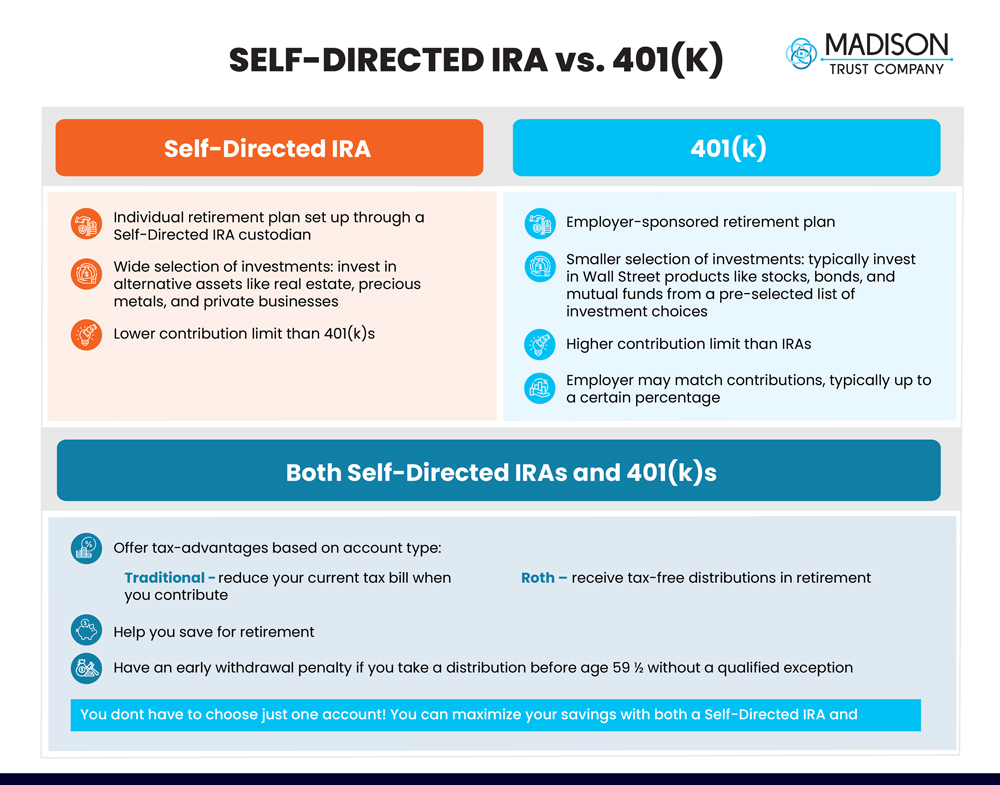

- Diversify Accounts: Use both 401(k) and IRA for flexibility in taxes and withdrawals.

- Review Beneficiaries and Fees: Ensure designations are updated and choose low-cost investments.

- Plan for Healthcare: Consider HSAs if eligible—triple tax advantages for medical costs in retirement.

- Stress-Test Your Plan: Use online calculators to simulate different scenarios.

Starting strong in 2026 sets you up for decades of security. What's your first retirement move this year? Share in the comments!

Disclaimer: Limits and rules current as of January 2026. This is informational only—not personalized financial advice. Consult a professional for your situation.

Comments

Post a Comment